A New Captain at the Fed: What the Kevin Warsh Nomination Means for Your Retirement

I’ve had a few of you reach out recently asking about the big news from Washington: the nomination of a new Chair for the Federal Reserve. It’s a great question because, while it might seem like just another political headline, the Federal Reserve (or "the Fed") is essentially the pilot of our economic airplane. When there’s a change in the cockpit, it’s natural to wonder if the flight will get a little bumpy.

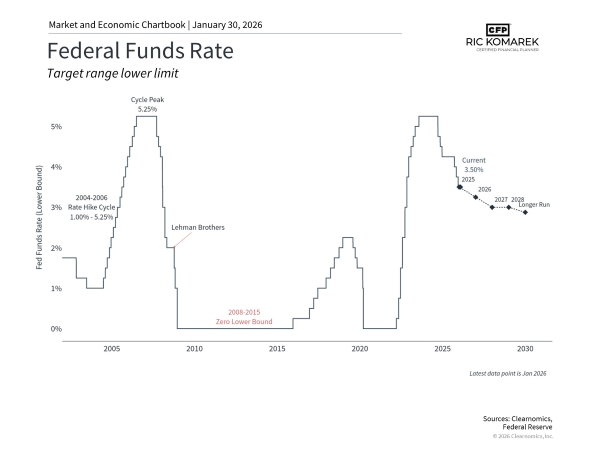

On January 30, it was announced that Kevin Warsh has been nominated to succeed Jerome Powell as the next Fed Chair. If confirmed by the Senate, he would take the reins in mid-May.

Who is Kevin Warsh?

You can think of Kevin Warsh as a veteran who’s been in the thick of it before. He served on the Fed’s board during the 2008 global financial crisis, which gives him a lot of experience when it comes to handling market turmoil.

In the past, he’s been known as an inflation hawk—someone who is very vigilant about keeping prices from rising too fast, often by keeping interest rates a bit higher. However, more recently, he has shared views that align with cutting rates to help spur the economy. He’s often described as a "markets guy" who understands how Wall Street and Main Street connect.

Why This Matters for Your "Financial House"

When we talk about the Fed, we’re really talking about two things that affect your retirement daily: interest rates and stability.

The Interest Rate Seesaw: Generally, when the Fed cuts rates, it’s like putting high-octane fuel in the economic engine. It can help the stock market and make borrowing cheaper. But for those of us relying on interest from savings or CDs, lower rates mean the "yield" on our cash might shrink.

The Inflation Guardrail: If the Fed cuts rates too fast or too deep, it can accidentally spark inflation. For a retiree, inflation is like a "hidden tax" that eats away at your purchasing power. We want a Fed Chair who can find that "Goldilocks" zone—not too hot, not too cold.

A Group Effort: It's important to remember that the Chair doesn't act alone. They are the quarterback of the team, but there’s a whole group (the Federal Open Market Committee) that votes on what to do. One person can’t move the needle single-handedly without building a consensus.

Navigating the Uncertainty

Right now, there is a bit of noise in the background, including legal investigations involving current Fed officials and debates in the Senate. This can create "headline stress," but history shows us that markets are remarkably resilient. They have performed well under many different leaders and political climates because they ultimately react to the strength of the economy, not just who is sitting in the big chair.

My Advice: Stay the Course

When the news gets loud, the best thing you can do is focus on your own financial fingerprint. Your plan was built to withstand changes in leadership and shifts in policy.

Think of this transition like a scheduled maintenance check on a bridge you’re crossing. It might cause a little lane closure or some slow traffic today, but the bridge itself—your long-term investment strategy—is built on a solid foundation.

Maintaining a disciplined, long-term approach is still the best way to move toward that goal of peace of mind.