Demystifying Medicare: How to Protect Your Financial House from Surprise Healthcare Costs

You’ve worked hard for decades to build a strong and comfortable financial house for your retirement years. You've carefully laid the foundation and built up your savings to provide shelter and support for the rest of your life. That is a massive achievement!

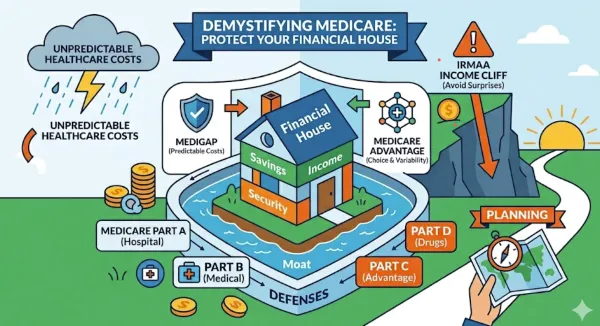

But as we transition into retirement, our focus has to shift. Even the best-built house needs a solid roof and a defensive moat to protect it from unexpected storms. When it comes to retirement planning, one of the biggest potential storms we face is healthcare.

As we age, healthcare often becomes our largest and most unpredictable expense. By the time folks reach 85, average out-of-pocket and covered healthcare spending can surge past $35,000 a year. Medicare is designed to help shoulder this burden, but the rules are notoriously confusing. If we don't navigate them carefully, surprise costs can easily breach your defenses.

Let’s break down how Medicare works and how we can proactively protect what you’ve built.

The ABCs (and Ds) of Medicare

A common misconception I hear is that Medicare will be entirely free because you’ve paid into it through payroll taxes your whole career. While part of it is covered, premiums and out-of-pocket costs can add up quickly.

Here is how the four main parts of the program work:

Part A (Hospital Insurance): This covers inpatient hospital stays, skilled nursing, and hospice care. For most folks who have worked and paid Medicare taxes for at least ten years, Part A is premium-free.

Part B (Medical Insurance): This covers physician visits, outpatient care, and preventive services. Part B requires a monthly premium, which can increase based on your income.

Part C (Medicare Advantage): These are bundled plans offered by private insurers as an all-in-one alternative to Original Medicare (Parts A and B). They often include extras like dental, vision, and hearing.

Part D (Prescription Drugs): This is optional, private insurance that helps cover the cost of your prescription medications. Like Part B, the premiums for Part D are tied to your income level.

Beware the Medicare Income Cliff

One of the biggest surprises that catches retirees off guard is a surcharge known as IRMAA, which stands for the Income-Related Monthly Adjustment Amount. If your income is too high, the government tacks this extra charge onto your Part B and Part D premiums.

For 2026, IRMAA kicks in if your Modified Adjusted Gross Income (MAGI) is over $109,000 as a single filer or $218,000 as a married couple filing jointly.

Here is why this is so dangerous: unlike standard tax brackets where only the income above a certain line is taxed at a higher rate, IRMAA is a cliff. If you go over the threshold by even a single dollar, you trigger the full surcharge for that entire bracket. This can mean hundreds or even thousands of dollars in surprise premium hikes.

To make matters trickier, Medicare uses a two-year lookback period. The surcharges you pay at age 65 are based on your tax return from when you were 63. This means the financial moves you make before you even retire—like realizing capital gains, executing Roth conversions, or taking a large withdrawal—can inadvertently push you off the IRMAA cliff.

This is why we want to look at your income strategy years in advance. Strategies like timing your Roth conversions carefully or using Qualified Charitable Distributions (QCDs) to satisfy your Required Minimum Distributions (RMDs) without raising your taxable income can help keep you safely below the cliff.

Choosing Your Defenses: Medigap vs. Medicare Advantage

When you enroll, you face a critical fork in the road: do you stick with Original Medicare and buy a Medigap policy, or do you choose a Medicare Advantage plan? This choice comes down to your personal risk tolerance and desire for predictability.

Medigap (Medicare Supplement Insurance): Think of this as paying for peace of mind. You pay a higher, fixed monthly premium to a private insurer, but in return, the plan helps cover your deductibles, copays, and coinsurance. Your out-of-pocket costs are lower and highly predictable. You also get nationwide coverage, which is fantastic if you plan on traveling in retirement.

Medicare Advantage (Part C): Think of this as a pay-as-you-go approach. The upfront monthly premiums are often very low (sometimes zero), but you take on more variable risk. You will face network restrictions, referral requirements, and higher out-of-pocket costs when you actually need care, up to an annual cap.

If you have a chronic condition, prioritize budget certainty, or plan to travel frequently, the predictable nature of Medigap is often worth the higher premium. If you have substantial cash reserves—like a healthy Health Savings Account (HSA)—and don't mind navigating network rules, Medicare Advantage might be a fit. Just be aware that switching from Advantage back to Medigap later in life can be incredibly difficult due to medical underwriting.

Your Medicare Plan is a Living Document

Building your retirement defenses isn't a set-it-and-forget-it event. Medicare requires an annual review. Every year, plan benefits change, premiums adjust, and the IRMAA thresholds shift. Your own health and income will also evolve.

Missing your Initial Enrollment Period (the seven-month window around your 65th birthday) can trigger permanent late penalties. Major life events like retirement, the loss of a spouse, or a sudden change in income can also open up special enrollment windows or give you grounds to appeal an IRMAA surcharge.

By understanding how these moving parts fit together, we can actively manage your healthcare costs, protect your savings, and give you the peace of mind to actually enjoy the retirement you’ve worked so hard to build.