Navigating the Fed's Next Chapter: What a Leadership Change Means for Your Retirement

You have likely been seeing headlines recently about changes coming to the Federal Reserve, specifically that Jerome Powell’s time as Fed Chair is coming to an end. It looks increasingly likely that Kevin Warsh will step into the role.

When you are retired or closing in on retirement, hearing about shifts at the highest levels of our financial system can feel a bit unsettling. You might be wondering how this affects your hard-earned savings. Let's sit down and walk through exactly what this means, minus the confusing Wall Street jargon.

The Quarterback of the Economy

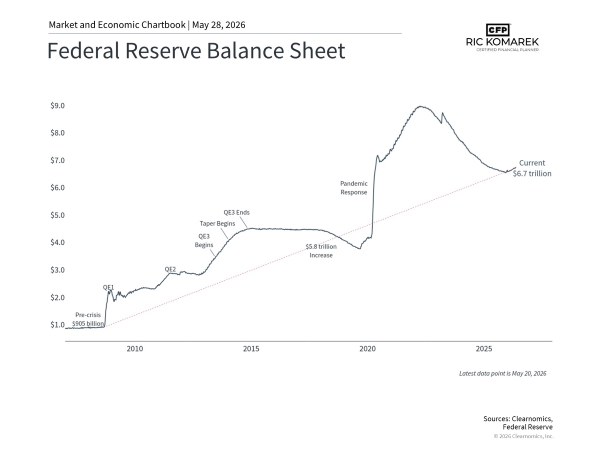

First, let's briefly review what the Federal Reserve actually does. Think of the Fed as the quarterback of the U.S. economy. They call the plays on monetary policy, which primarily means they control the money supply and set short-term interest rates. Their main goals are to keep employment high and inflation in check.

Under Jerome Powell, we saw a period of historic challenges. The Fed initially viewed post-pandemic inflation as temporary, which led to a delay in raising interest rates. When they finally did, they had to raise them aggressively to catch up.

Enter Kevin Warsh: A Different Approach

If Kevin Warsh takes over, we can expect a shift in strategy. Warsh previously served on the Federal Reserve Board of Governors from 2006 to 2011 and has a background in investment banking.

In financial circles, Warsh is considered hawkish. This simply means he is generally more concerned with fighting inflation than he is with keeping interest rates low to stimulate growth. He has been a vocal critic of the way the Fed handled recent inflation. Here are a few key ways his leadership might look different:

Higher Rates for Longer: Warsh is less likely to slash interest rates quickly. He tends to favor a more traditional approach where rates stay elevated to ensure inflation is truly defeated.

A Higher Inflation Target: He has suggested that the Fed's strict 2% inflation target might be arbitrary, and he might be comfortable letting inflation hover slightly higher, perhaps around 3%, if it means a healthier overall economy.

Removing the Safety Net: For years, Wall Street has relied on something called the Fed put—the idea that if the stock market starts to crash, the Fed will swoop in and lower interest rates to rescue it. Warsh is much less likely to intervene just to prop up the stock market. He believes markets should function on their own fundamentals.

What This Means for Your Retirement

So, how does a Warsh-led Fed impact your portfolio?

Without the Fed rushing to rescue the markets at the first sign of a dip, we might see more day-to-day volatility in stock prices. The era of "free money" and near-zero interest rates is likely behind us for now. However, higher interest rates aren't inherently bad news for retirees. In fact, they mean that conservative investments like bonds and high-yield savings accounts can actually generate meaningful, reliable income for your portfolio again.

Keeping Your Financial House Strong

Whenever there is a major shift in the economic winds, the key is not to panic or make sudden, emotional changes. Think of the retirement income plan we've built as your financial house. We designed it with a strong foundation to weather all kinds of economic seasons—including changes in Washington.

Here is how we stay on track:

Stick to the Plan: We don't try to time the market based on who is sitting in the Fed Chairman's seat. Your plan is built around your personal life goals, not short-term headlines.

Embrace Diversification: Because the stock market might be a bit bumpier, having a well-diversified portfolio is more important than ever.

Focus on the Controllables: We can't control interest rates, but we can control our asset allocation, our withdrawal rates, and our long-term perspective.

Transitions in leadership always bring a degree of uncertainty, but your financial security shouldn't rely on guesswork. We will continue to monitor these changes and adjust your strategy if necessary, always keeping your peace of mind front and center.