Seed or Harvest? A Strategic Guide to Roth Decisions in Retirement

One of the most common questions I hear from people planning for retirement revolves around Roth accounts. The idea of tax-free growth is incredibly appealing, and for good reason! But it brings up a fundamental choice: should you pay your taxes now or pay them later?

I often describe it like this: a Traditional IRA or 401(k) is like paying tax on the harvest. You get a tax break on the money you put in (the seed), but you pay taxes on everything you withdraw later—the seed and all the growth. A Roth account is the opposite; you pay tax on the seed. There’s no upfront tax break, but your withdrawals in retirement—the entire harvest—are completely tax-free.

This sounds simple enough, but deciding which path to take isn’t a one-time decision. The right answer can change from year to year. The real power is in understanding the details and making strategic choices along the way.

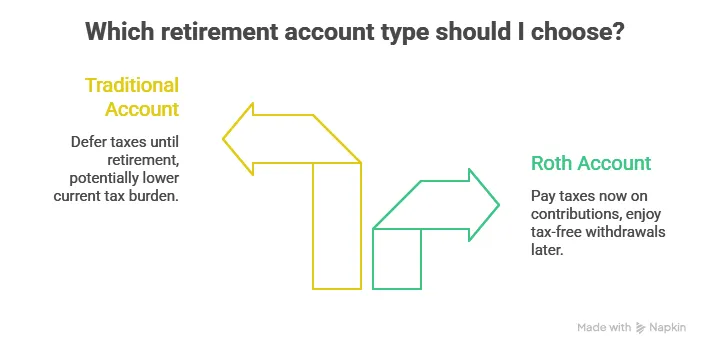

Is a Roth Contribution Right for You This Year?

The simple rule of thumb is this: a Roth makes the most sense when you believe your tax rate today is lower than it will be in the future.

Think about a teenager with their first summer job. They have earned income but are likely in a 0% federal tax bracket. For them, a Roth contribution is a fantastic move. They pay no tax on the "seed," and that money can grow for decades, eventually becoming a tax-free "harvest."

On the other hand, someone in their peak earning years, say in the 32% or 35% federal bracket and living in a high-income-tax state, might benefit more from a traditional, tax-deductible contribution. They can use that immediate tax deduction to lower their bill today, assuming their tax rate will be lower when they start making withdrawals in retirement.

The Strategic Power of Partial Roth Conversions

A Roth conversion is the process of moving money from a traditional (pre-tax) account to a Roth (after-tax) account. When you do this, you have to pay ordinary income tax on the amount you convert in that year. So, why would anyone volunteer to pay taxes sooner than they have to? It's all about strategy, especially when thinking about the next generation.

Let’s imagine a couple, Sarah and Tom. They are comfortably in the 24% tax bracket in retirement. Their son, their sole beneficiary, is a successful surgeon in the 37% tax bracket. If Sarah and Tom leave him their large traditional IRA, he will have to withdraw all of it within 10 years of their passing (due to the "10-year rule" for most non-spouse beneficiaries) and pay taxes at his very high 37% rate.

Instead, Sarah and Tom could strategically convert portions of their IRA to a Roth each year, paying taxes at their lower 24% rate. When their son inherits the Roth IRA, the 10-year rule still applies, but every dollar he withdraws is completely tax-free. They essentially paid the tax bill for him, but at a much lower rate.

Why a Conversion Isn't Always the Answer

While conversions can be powerful, they aren’t a magic bullet. Paying a tax bill today with real dollars requires careful thought. If your current tax rate is already in the 22% or 24% bracket, the math gets a little fuzzier. You're paying a significant tax bill now in the hope that you'll avoid a higher one later.

But what if your future tax rate isn't as high as you expect? What if tax laws change? By converting, you "lock in" today's tax rate on that money. Sometimes, it can be better to keep your options open. For example, if you are charitably inclined, once you turn 70 ½, you can make Qualified Charitable Distributions (QCDs) directly from your traditional IRA. This allows you to meet your Required Minimum Distributions (RMDs) without that money ever showing up as taxable income. It’s another powerful tool in the toolbox that you give up on any money you convert to a Roth.

Looking Beyond the Tax Bracket: The Ripple Effect

Perhaps the most overlooked aspect of a Roth conversion is what I call the ripple effect. Your tax bracket alone doesn’t tell the whole story. A conversion can create ripples that touch other parts of your financial life, changing your true marginal tax rate.

Here are two key examples:

Taxation of Social Security: The amount of your Social Security benefit that is taxable depends on your other income. A large Roth conversion increases your income for that year, which could cause more of your Social Security benefits to become taxable. That's a hidden tax increase.

Medicare Premiums (IRMAA): Your Medicare Part B and D premiums are based on your income from two years prior. A large conversion could push you over an income threshold, triggering a significant surcharge called the Income-Related Monthly Adjustment Amount (IRMAA). This is a very real cost that needs to be factored into the decision.

The ripple effect can also work in your favor. By having a pot of tax-free Roth money, you can draw from it strategically in retirement to keep your income below those key thresholds, potentially reducing the tax on your Social Security or avoiding IRMAA surcharges altogether.

Putting It All Together: Your Financial Fingerprint

As you can see, a smart Roth strategy is about more than just a single account; it’s about how all the pieces of your financial life fit together. Your situation is unique—it’s your financial fingerprint. A proper analysis of a Roth conversion shouldn't happen in a vacuum. It must be comprehensive and answer key questions:

Does the plan account for all your assets and income sources?

Does it project how inflation will impact future tax brackets and those critical IRMAA thresholds?

For married couples, does it model what happens when one spouse passes away and the surviving spouse becomes a single tax filer?

Does it consider the likely tax situation of your beneficiaries?

Ultimately, the decision to make Roth contributions or conversions is not a one-and-done event. It's a flexible, year-by-year strategy that adapts to your life. By carefully weighing the trade-offs each year, you can build a more resilient retirement income plan and a more powerful legacy for the ones you love