Understanding Rising Insurance Costs: What's Driving Up Your Bills?

If you've been opening your auto and homeowners insurance bills lately and feeling a bit of sticker shock, you're definitely not alone. Here in Redding, and across the country, we're seeing a significant surge in property and casualty insurance premiums that's outpacing the general rate of inflation. It's a topic I know is on many of your minds, and it's crucial to understand what's behind these increases and what we can do about it.

Let's look at the scale of what's happening. Data from the Bank of America Institute, which tracks customer banking information, reveals that median auto and home insurance payments rose by a substantial 6% in the 12 months leading up to May 31st. But this isn't a one-time jump. It's built upon increases from previous years, leading to a cumulative rise of over 40% in median premium payments since June 2020! That's a significant chunk of our household budgets.

When we break it down further, homeowners insurance costs show a particularly wide range depending on where you live. According to Bankrate, the national average cost for $300,000 of dwelling coverage is around $2,341 per year. However, here in California, especially in areas prone to wildfires, many of you are likely seeing premiums well above that average. Consider Florida, where the average is a staggering $5,409, compared to a much lower $839 in a state like Vermont. These geographical differences highlight some of the key factors driving these increases.

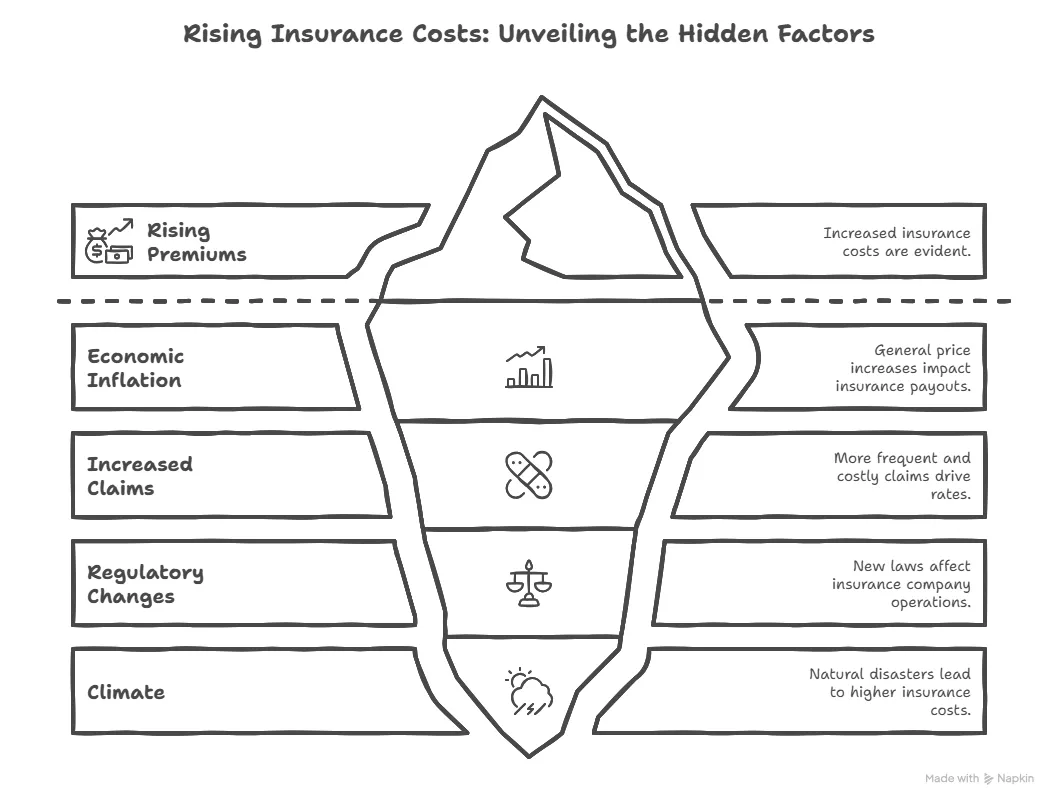

So, what exactly is causing this upward trend in insurance costs? While the broader inflation of goods has started to cool down, there's concern among experts that tariffs could lead to higher prices for materials used in housing and automobiles. This, in turn, would increase the cost to repair or rebuild after a loss, directly impacting what insurance companies have to pay out and, consequently, what they charge in premiums.

However, a major driver, particularly for us here in California and for those in other vulnerable regions, is the increasing frequency and severity of natural disasters. Clients living in areas with a higher risk of events like hurricanes (think of our friends in Florida) or wildfires (unfortunately, a reality we face here in the West) are experiencing some of the most significant premium hikes. In some extreme cases, insurance companies have even made the difficult decision to pull out of certain high-risk areas altogether, making it incredibly challenging, or even impossible, to obtain coverage. The data underscores this point: there have been 23 disasters in the United States with costs exceeding $1 billion each in just the past 5 years. If this pace continues, we may not see much relief from these rising insurance premiums anytime soon.

Now, how can I, as your financial advisor, help you navigate this challenging landscape? This trend actually presents some valuable opportunities for us to work together and find solutions.

One way I can assist is by helping you model different scenarios for these rising costs within your overall financial plan. For example, we can stress-test your plan by using a higher inflation rate specifically for insurance expenses compared to other living costs. This will give us a clearer picture of the potential impact on your retirement income and allow us to make any necessary adjustments proactively.

Another valuable service I offer is helping you explore options for less expensive insurance coverage that still adequately meets your needs. This might involve comparing quotes from different insurers or understanding the trade-offs of different coverage levels and deductibles. For example, increasing your deductible could lead to a lower premium, but we need to carefully consider your ability to comfortably cover that higher out-of-pocket cost in the event of a claim.

For those of you considering a move in retirement, I can also illustrate how your insurance costs might change if you were to relocate to a different area with a lower risk profile for natural disasters. This can be a significant factor to consider in your overall retirement planning.

Finally, I can help you think through the "right" amount of insurance coverage. This involves considering several factors, such as the percentage of your total wealth that a particular asset represents (for instance, your home), your personal tolerance for risk, and your financial capacity to absorb different levels of potential loss. There's a balance to be struck between adequate protection and managing your ongoing expenses.

Rising insurance costs are a real concern, but by understanding the factors driving these increases and proactively exploring your options, we can work together to mitigate their impact on your financial well-being. Don't hesitate to reach out so we can discuss your specific situation and develop a strategy that makes sense for you here in Redding.