Don’t Let Market Pullbacks Derail Your Retirement Journey

It’s completely natural to feel a knot in your stomach when you turn on the news and hear that the stock market is down. Right now, the S&P 500 has pulled back about 4% from its recent peak. When you are at or near retirement, watching your hard-earned nest egg fluctuate can be nerve-wracking.

When this happens, I like to remind my clients of a simple truth: investing is a lot like flying in a commercial airplane. When you hit turbulence, it can be uncomfortable, and your instinct might be to panic. But you don't jump out of the plane. You fasten your seatbelt, trust the design of the aircraft, and wait for smoother skies ahead.

How we react to these temporary market declines has a massive impact on your long-term financial success and your ultimate peace of mind. Here are a few key facts to help keep things in perspective.

Pullbacks are Completely Normal

Just like shifting weather patterns, market pullbacks are a natural part of the investing environment. History shows us that these dips happen all the time.

Since 1980, the S&P 500 has experienced an average of 4.6 pullbacks of 5% or more every single year.

Despite these regular drops, the market has delivered positive annual returns in the vast majority of those years.

Look at last year, for example. In 2025, the S&P fell roughly 19% right after the tariff announcements in April. It felt scary at the time, but the market rebounded and finished the year up a very strong 18%.

The Danger of Trying to Time the Market

When the market dips, you might be tempted to sell your investments, move to cash, and wait for things to "calm down." This is called market timing, and it is incredibly dangerous to your financial health.

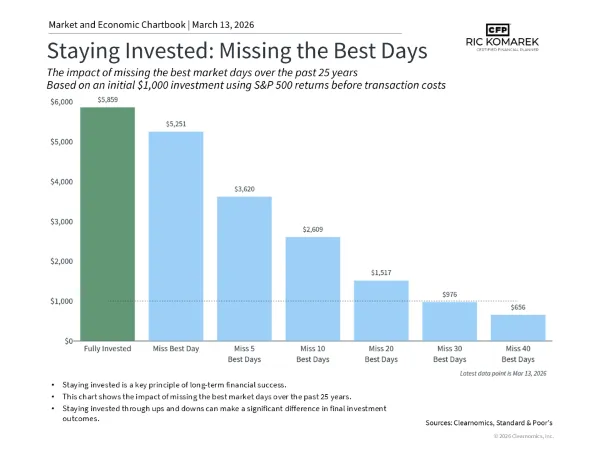

The problem is that the market's absolute best days almost always occur within days of its absolute worst days. If you pull your money out, you are highly likely to miss the rebound.

Data looking at the past 25 years paints a very clear picture of just how costly this can be. Let's look at what would happen to a hypothetical $1,000 investment in the S&P 500 over that 25-year period:

Fully Invested: If you left the money alone, it grew to $5,859.

Missing the 10 Best Days: If you tried to time the market and missed just the 10 best days over a quarter-century, your ending balance was more than cut in half, dropping to $2,609.

Missing the 30 Best Days: If you missed the 30 best days, you actually lost money over 25 years, ending up with just $976.

Missing just a handful of the best days can permanently damage the foundation of your financial house.

The Cost of Waiting on the Sidelines

On the flip side, what if you are holding cash right now and waiting for a bigger pullback before you invest? This, too, can be a costly mistake.

Based on market data going all the way back to 1927, if you sit in cash waiting for just a 5% drop to "buy the dip," you will sit on the sidelines for an average of 303 days. During that waiting period, you miss out on an average return of 13.8%.

Your Next Steps

Building a strong retirement plan means designing a strategy that can weather these normal market storms so you don't have to rely on guesswork. Maintain a long-term perspective, ignore the short-term noise, and stay focused on the life you want to live in retirement.