Private Assets in Your 401(k): New Opportunities and Potential Pitfalls

For decades, your 401(k) has likely been a familiar and steady part of your retirement planning journey. You contribute from your paycheck, maybe get an employer match, and invest in a mix of stocks and bonds, often through mutual funds. But the landscape of workplace retirement plans is starting to shift in a significant way, and it’s something you need to be aware of, especially as you navigate the critical years leading up to retirement.

There is a growing momentum to ease the rules around including private market investments—things like private equity, private real estate, and other alternative assets—in retirement plans like your 401(k). The rules that govern these plans are set by a law called the Employee Retirement Income Security Act, or ERISA, and recent government actions are paving the way for these changes.

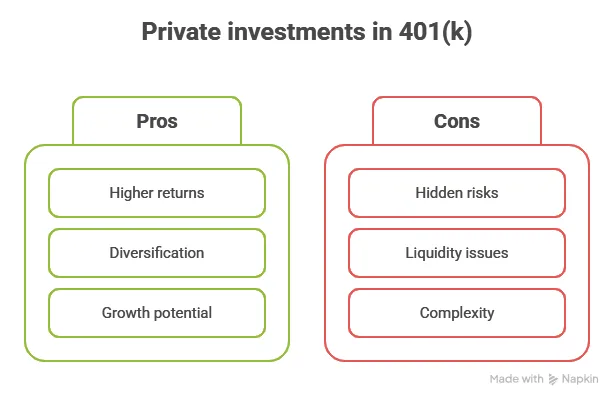

What’s the driving force behind this? Proponents argue that it could be a good thing. They believe it would allow a broader range of investors, like you and me, to access investments typically reserved for large institutions and the very wealthy. The idea is that this could provide greater diversification for your retirement savings by giving you a stake in private companies, not just those publicly traded on the stock market.

But with new opportunities come new questions and potential pitfalls.

How You Might Get This Exposure—Even Without Realizing It

Have you ever wondered what happens if you don't actively choose the investments in your 401(k)? Many companies now use "auto-enrollment" to get employees started, and they often place your money into a default option, which is typically a target-date retirement fund. These funds are designed to be a simple, one-stop solution, automatically adjusting their mix of stocks and bonds to become more conservative as you get closer to your target retirement date.

Traditionally, these funds have stuck to publicly traded investments. However, with this new push, we could start seeing private equity funds and other alternatives included in their asset mix. This means that if you are in your company’s default target-date fund, you might soon have exposure to these complex assets without ever making a conscious decision or even realizing the change has been made.

The Potential Pitfalls and Challenges

While the idea of greater diversification sounds appealing, the inclusion of private assets in a 401(k) comes with some serious considerations.

For You, the Investor:

Higher Fees: Private equity funds almost always come with much higher management fees than the low-cost index funds commonly found in 401(k) plans. These higher expenses can eat away at your returns over time, creating a drag on your nest egg’s growth.

Different Risk Profile: These are not your typical stocks and bonds. Private assets often have different characteristics when it comes to risk, volatility, and liquidity (meaning how easily they can be bought or sold). This might not be an attractive or appropriate addition, especially for investors who were automatically enrolled and may not understand the new risks they are taking on.

For Your Advisor (That's Me):

The shift also creates new challenges for financial advisors. My primary responsibility is to act as your fiduciary, always putting your best interests first. The inclusion of these complex and sometimes opaque assets in standard 401(k) funds makes that job more challenging. Industry observers are concerned about potential legal exposures from high-fee funds that underperform, which could draw lawsuits. It increases my responsibility to perform deep due diligence on every fund offered in a plan to ensure it's appropriate for my clients.

My Crucial Role as Your Guide

This is precisely where a trusted financial advisor becomes so important. While these changes might seem confusing, my job is to bring clarity to your financial life. This new trend offers a perfect opportunity for me to help you:

Understand Your Holdings: We can dig into your 401(k) statements and find out what you really own. If your target-date fund now includes private assets, you deserve to know about it.

Determine if It's Appropriate: Together, we can determine whether this new investment mix is suitable for your specific financial situation, your timeline to retirement, and your personal risk tolerance.

Suggest Alternatives: If the default option in your 401(k) no longer aligns with your goals, I can help you explore other funds within your plan to create an asset allocation that you are comfortable with and that serves your best interests.

The world of investing is always evolving. The key is not to be alarmed, but to be aware and proactive. If you’re concerned or just curious about how these potential changes could impact your retirement savings, let’s schedule a time to review your 401(k).