The Gas Pump Premium: Why Market Swings Aren't a Reason to Tear Up Your Retirement Plan

The Noise at the Pump

It is easy to feel a bit of whiplash when looking at the financial headlines lately. On one hand, the broader stock market has been hitting new all-time highs, powered by solid corporate earnings and a resilient economy. On the other hand, we are seeing sudden swings in major technology stocks and renewed chatter about rising inflation.

When you are at or near retirement, these mixed signals can naturally trigger a nagging fear: Is my hard-earned nest egg safe, or am I about to make a costly mistake? Much of the recent anxiety boils down to uncertainty around the Federal Reserve and interest rates. After some strong employment data and a jump in the Consumer Price Index, some investors started worrying that the Fed might raise rates again. But if we pull back the curtain on the inflation numbers, the reality is far more reassuring than the evening news suggests.

Stripping Away the Headlines

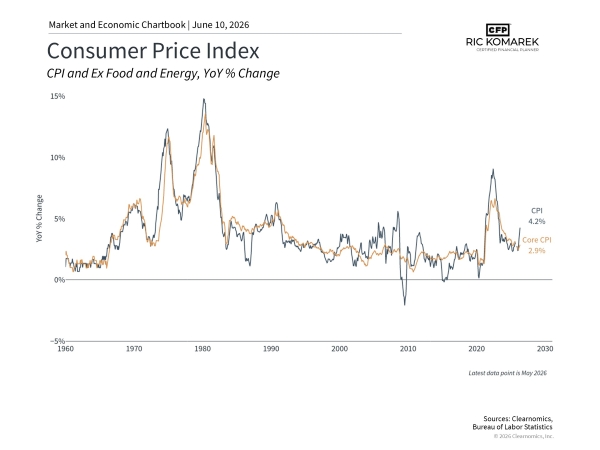

Yes, inflation ticked up to 4.2% year-over-year in the latest May data. But a single look under the hood shows exactly where that pressure is coming from.

Headline inflation sits at 4.2%, but when you take out volatile food and energy costs, that number drops to 2.9%. Strip out housing costs as well, and prices only rose 2.4%.

What does this tell us? It means the pain we are feeling is highly concentrated. Paying over $4 a gallon for gasoline is a genuine frustration for households, but these price spikes have not spread broadly across the rest of the economy.

So why does this cause major technology stocks to swing so wildly?

Future Value: Investors buy fast-growing tech companies because they expect big profits far down the road.

The Interest Rate Scale: When interest rates threaten to go up, those future profits are mathematically worth less today.

The Rollercoaster Effect: Even a tiny shift in interest rate expectations can cause these giant stocks to swing sharply, dragging the broader market sentiment with them.

We saw this exact movie play out recently. The group of massive tech giants commonly referred to as the "Magnificent 7" lost roughly half their value when inflation heated up a few years ago, only to roar back to new highs as soon as rates stabilized. Swings are a feature of these stocks, not a bug.

The Shiny Object of Shiny New Stocks

At the same time, this strong market has brought a wave of high-profile initial public offerings (IPOs)—specifically companies deeply tied to artificial intelligence.

While it is exciting to see new, innovative companies join the public market, retirement planning requires a different perspective on these events:

The Ground Floor is Crowded: By the time a massive company finally goes public, institutional insiders have already captured much of the early, explosive growth.

Lock-Up Periods: Insiders are usually restricted from selling immediately, meaning early trading can be incredibly volatile.

History Repeats: We saw massive waves of IPO enthusiasm in the late 1990s and again during the post-pandemic boom. Both waves eventually cooled.

The good news for your retirement portfolio? You do not need to gamble on single stock offerings. Broad market indexes automatically adopt these successful new companies over time as they grow, giving you a piece of the action safely and gradually.

Protecting Your Financial House

When you are in or near retirement, your portfolio acts as a financial moat, designed to protect your lifestyle from temporary economic storms.

Even if the Fed does adjust interest rates later this year, the projected move is minor—a mere 0.25% tweak. Compare that to the massive, rapid rate hikes we successfully navigated recently, and it becomes clear that this is a minor ripple, not a tidal wave. History shows us that the markets can thrive in many different interest rate environments, provided the underlying economy stays healthy.

Market swings are entirely normal, and often healthy. Neither a spike in gas prices nor the hype around new tech stocks is a reason to fundamentally alter a carefully constructed, long-term plan built around your life goals.

With all the moving pieces in the world today, are you confident that your current strategy is built to withstand short-term noise while securing your long-term peace of mind?

If you want to dive deeper into managing these critical years leading up to and through retirement, I highly recommend reading The Retirement Red Zone. It offers a practical roadmap for protecting your financial house when it matters most. Of course, if you ever want to chat through how these recent headlines impact your specific goals, my door is always open.