The Social Security COLA: What It Is, and Why It's Not Enough

Every fall, usually in October, you’ll see headlines about the Social Security Administration announcing the "COLA" for the upcoming year. It often gets talked about as a "raise" for retirees, and when the number is high, it makes big news.

But is it really a raise? And more importantly, how does it actually fit into your long-term retirement income plan?

A lot of people are aware of COLA, but I find they don't always understand the full impact it has on their planning, both before and after they start taking benefits. Let's break it down in simple terms.

💰 What Exactly Is COLA?

COLA stands for Cost-of-Living Adjustment.

Think of it this way: COLA isn't a pay raise; it's an adjustment to help you keep up. It’s an increase applied to your Social Security benefits specifically designed to counteract the effects of inflation.

When prices for groceries, gas, and healthcare go up, your Social Security benefit is supposed to go up with them. The goal is to help you maintain your standard of living and purchasing power, not to increase it.

The adjustment is calculated by comparing average prices from the third quarter of one year to the third quarter of the previous year. For example, the Hartford Funds article I reviewed noted the 2026 COLA is projected to be 2.8%. This would take an average retired worker's benefit from $2,015 to about $2,071.

That $56 bump is helpful, but it's crucial to understand when COLA starts affecting your personal benefit.

🗓️ How COLA Affects Your Benefits at Different Ages

This is a key part of your claiming strategy that often gets overlooked. The COLA math doesn't just start when you file for benefits.

Before You Turn 62

Before age 62, COLA doesn't really factor into your benefits, so there's no need to stress about it.

From Age 62 Onward (This is the important part!)

Age 62 is the magic number. This is the earliest age you can claim Social Security, though I often caution clients to think hard about this. Filing early (any time before your Full Retirement Age, or FRA) means you are locking in a permanently reduced monthly benefit for the rest of your life.

Here’s the key: COLA adjustments begin applying to your benefits starting at age 62, even if you don't claim them.

These annual inflation increases are factored into your benefit calculation from age 62 onward. This means that by waiting to claim, you not only get a higher base benefit, but that benefit has also been growing with all the COLAs announced since you turned 62.

Waiting Past Full Retirement Age (FRA)

If you wait past your FRA (up to age 70), you get a double win. You receive:

Delayed Retirement Credits: This is an extra percentage added to your benefit for every year you wait past your FRA (up to age 70).

All the COLAs: You also get the benefit of all the COLA increases that have happened since you were 62.

This combination is what can make delaying your Social Security claim so powerful, as it locks in a much higher, inflation-adjusted "personal pension" for the rest of your life.

⚠️ The COLA "Gotcha": Why It's Not a Full Retirement Plan

Here's the part I really want to focus on as your planner. While COLA is a nice feature, it is not a plan. It’s a patch.

A recent article from The Motley Fool, cited by Hartford Funds, really highlights this. It stated that while the average 67-year-old retiree gets about $25,956 per year from Social Security, most retirees need roughly $75,020 a year to live comfortably.

That’s a massive gap.

The COLA adjustment only applies to the $26,000 part, not the whole $75,000 you might need.

Focus on What You Can Control

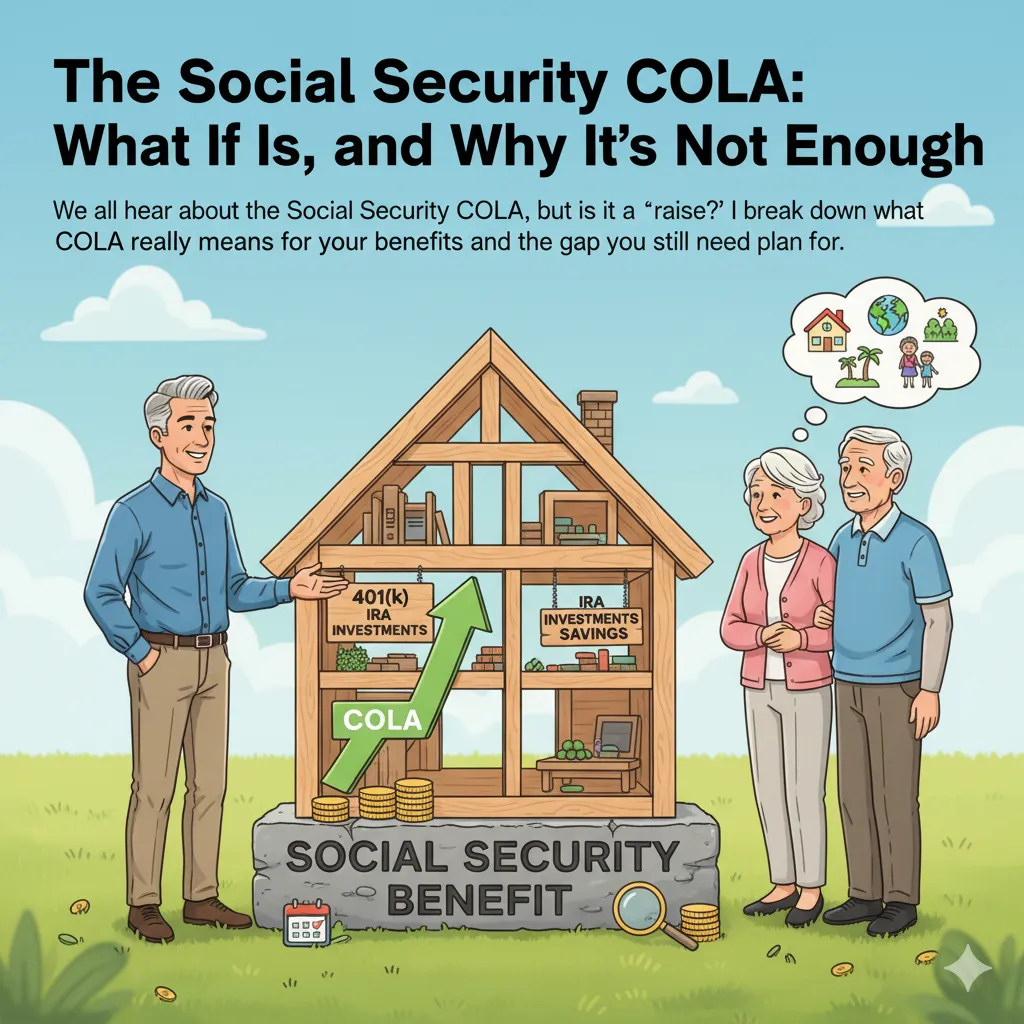

This is where we bring it back to your financial house.

Think of your Social Security benefit as the strong foundation. The COLA adjustments are like routine maintenance—they help protect that foundation from eroding due to the "weather" of inflation.

But COLA doesn't build the rest of the house.

You can't control what the COLA rate will be next year. You can't control inflation or the stock market.

What can you control?

Your savings strategy.

Your investment decisions.

Your withdrawal plan in retirement.

How you coordinate income from your 401(k)s, IRAs, and other brokerage accounts to fill that gap.

This is where real planning comes in. We work together to build the rest of your financial house—the walls, the roof, the plumbing—so that you have a comfortable, secure retirement. We build a plan that is designed for your goals, not one that just relies on a small inflation adjustment from the government.