Weathering the Headlines: Why Staying Invested is Your Strongest Defense

It has been an eventful period for financial markets and geopolitics, and I want to take a moment to share some perspective on what it all means for your long-term financial plan.

Think of your retirement portfolio like a sturdy, well-built house. You’ve designed it to provide comfort and security for decades, focusing on ensuring the income it generates can last for your entire lifetime. But even the strongest house will occasionally face fierce, unexpected storms. Right now, between the evolving conflict in the Middle East and recent market volatility, it might feel like the wind is howling outside.

Despite these uncertainties, the stock market has actually reached several new all-time highs this year. These rapid swings serve as a perfect reminder of how quickly market conditions can change, and why maintaining a steady, long-term approach remains the foundation of your financial security.

The Surprise of Market Recoveries

One of the most consistent lessons I've learned from financial history is that markets have a way of surprising us. They often rebound exactly when investors are feeling the most pessimistic.

We saw a great example of this recently. At its lowest point in March, the S&P 500 had declined about 9%. But as positive news emerged, markets began to recover, resulting in a 12% rebound during the first three weeks of April.

When you see the market dip, the natural human instinct is to run for cover—to pull your money out and wait for the "storm" to pass. But trying to time the market is incredibly difficult and often counterproductive. Investor sentiment tends to be at its absolute worst right before markets begin to recover.

We saw this exact same dynamic play out last year when the S&P 500 fell nearly 19% due to tariff concerns. Many feared a deep recession was inevitable. Fortunately, that didn't happen, and markets recovered. Those who stayed safely inside their financial house and remained invested were rewarded.

The Cost of Missing the Best Days

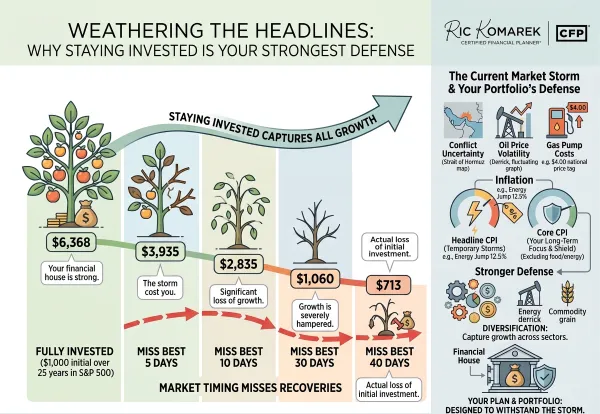

To put the danger of market timing into perspective, let's look at the numbers. Over the past 25 years, if you had invested $1,000 in the S&P 500 and simply left it alone, your investment would have grown to $6,368.

But what if you had tried to dodge the bad days and inadvertently missed out on the market's strongest recovery days? The impact is staggering:

Missing just the 5 best days drops your total to $3,935.

Missing the 10 best days cuts your balance down to $2,835.

Missing the 40 best days leaves you with just $713—meaning you actually lost money over a 25-year period.

This isn't to say that markets always bounce back overnight, but history clearly shows that reacting to short-term volatility by moving to the sidelines can be incredibly costly to your retirement nest egg.

Current Developments and Your Wallet

The recent swings in the stock market are closely tied to the situation in Iran and the Strait of Hormuz. Because of this, oil prices have been on a roller coaster, swinging from the mid-$80s per barrel to as high as $118.

For everyday consumers, this shows up right at the gas pump. With the national average for regular unleaded settling around $4.00 per gallon—about a dollar above where it was before the conflict—filling up your car takes a bigger bite out of your budget.

This naturally leads to concerns about higher inflation. The latest Consumer Price Index (CPI)—a tool economists use to measure the average change in prices we pay for everyday goods—confirms these challenges. In March, energy prices jumped 12.5% compared to last year.

However, there is an important silver lining. "Core inflation," which simply looks at the economy but excludes the volatile, roller-coaster prices of food and energy, rose only 2.6%. This tells us that higher energy costs haven't broadly infected the rest of the economy just yet. Economists often view these types of supply-driven price shocks as temporary.

What This Means for Your Financial Plan

I know that seeing prices rise at the pump and watching the news can bring up very real fears about outliving your money. But I want to reassure you: this is exactly why we built your plan the way we did.

The possibility of inflation underscores the importance of having a portfolio that can not only generate sufficient income for today but also grow to protect your purchasing power tomorrow. Your well-constructed portfolio isn't built around predicting which specific areas of the market will win on any given day. Instead, it’s designed to capture the growth of all parts of the market over time. For example, energy-related sectors and commodities have been strong performers recently, helping to balance out other areas.

We don’t know exactly what the headlines will say next month, but your financial plan is built to withstand these environments.

As always, if you have questions or would simply like to talk through how any of this relates to your specific situation and peace of mind, please feel free to reach out. I am always here to help.